Spurious Regression - Visualization -II

Simulate the regression statistics between 2 random walks

> set.seed(1977)

> N <- 100

> coefs <- numeric(0)

> tstat <- numeric(0)

> ssd <- numeric(0)

> for (i in 1:1000) {

+ y <- cumsum(rnorm(N))

+ x <- cumsum(rnorm(N))

+ fit.sum <- summary(lm(y ~ x))

+ coefs <- c(coefs, coef(fit.sum)[2, 1])

+ tstat <- c(tstat, coef(fit.sum)[2, 3])

+ }

> length(which(abs(tstat) > 1.96))/1000

[1] 0.76 |

77 percent of the times you would tend to reject the null hypothesis.

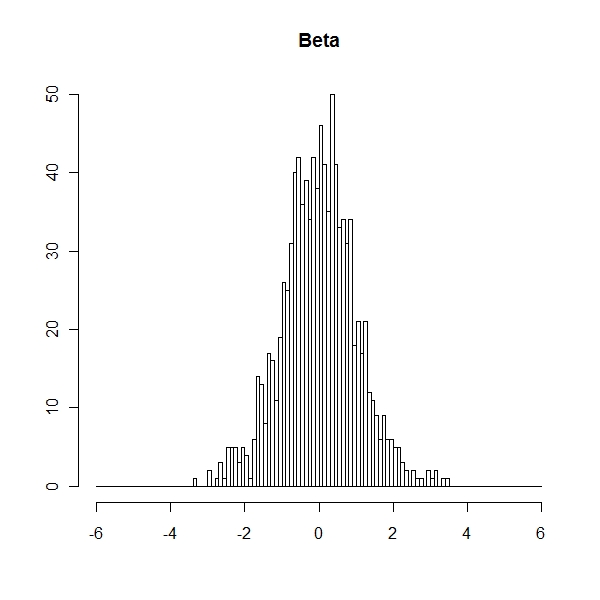

Frequency Histogram of t value

> sample.mean <- mean(coefs) > sample.sd <- sd(coefs) > hist((coefs - sample.mean)/sample.sd, breaks = seq(-6, 6, 0.1), + main = "Beta", xlab = "", ylab = "") |

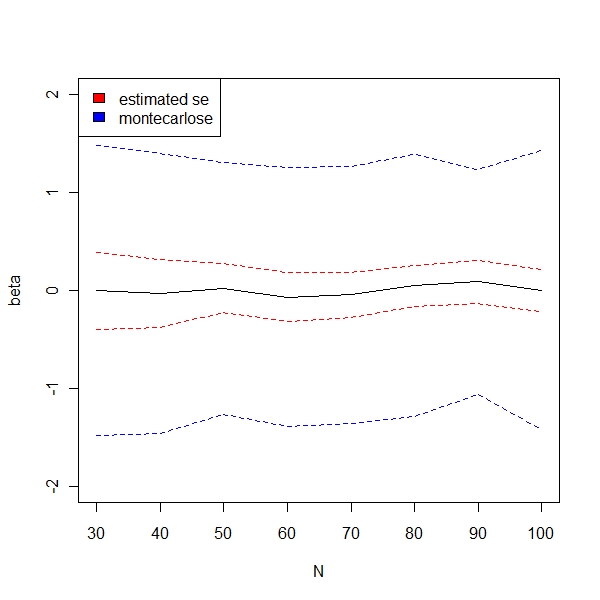

Montecarlo Sigma is actually higher than the reported standard error

> N <- seq(30, 100, 10)

> k <- 1

> coefs <- numeric(0)

> tse <- numeric(0)

> mcse <- numeric(0)

> tstat <- numeric(0)

> tstat.sd <- numeric(0)

> probs <- numeric(0)

> for (k in seq_along(N)) {

+ print(k)

+ coefs.temp <- numeric(0)

+ tse.temp <- numeric(0)

+ tstat.temp <- numeric(0)

+ for (i in 1:100) {

+ y <- cumsum(rnorm(N[k]))

+ x <- cumsum(rnorm(N[k]))

+ fit.sum <- summary(lm(y ~ x))

+ coefs.temp <- c(coefs.temp, coef(fit.sum)[2, 1])

+ tse.temp <- c(tse.temp, coef(fit.sum)[2, 2])

+ tstat.temp <- c(tstat.temp, coef(fit.sum)[2, 3])

+ }

+ sample.mean <- mean(coefs.temp)

+ sample.sd <- sd(coefs.temp)

+ coefs <- c(coefs, sample.mean)

+ mcse <- c(mcse, sample.sd)

+ tse <- c(tse, mean(tse.temp))

+ tstat <- c(tstat, mean(tstat.temp))

+ tstat.sd <- c(tstat.sd, sd(tstat.temp))

+ probs <- c(probs, length(which(abs(tstat.temp) > 2))/100)

+ } |

> plot(N, (coefs), type = "l", ylim = c(-2, 2), ylab = "beta")

> points(N, (coefs) + 2 * (mcse), type = "l", lty = "dashed", col = "blue")

> points(N, (coefs) - 2 * (mcse), type = "l", lty = "dashed", col = "blue")

> points(N, (coefs) + 2 * (tse), type = "l", lty = "dashed", col = "red")

> points(N, (coefs) - 2 * (tse), type = "l", lty = "dashed", col = "red")

> legend("topleft", legend = c("estimated se", "montecarlose"),

+ fill = c("red", "blue")) |

One can clearly see that montecarlo se remains high even as n increases And t stat error severely underestimates the mean

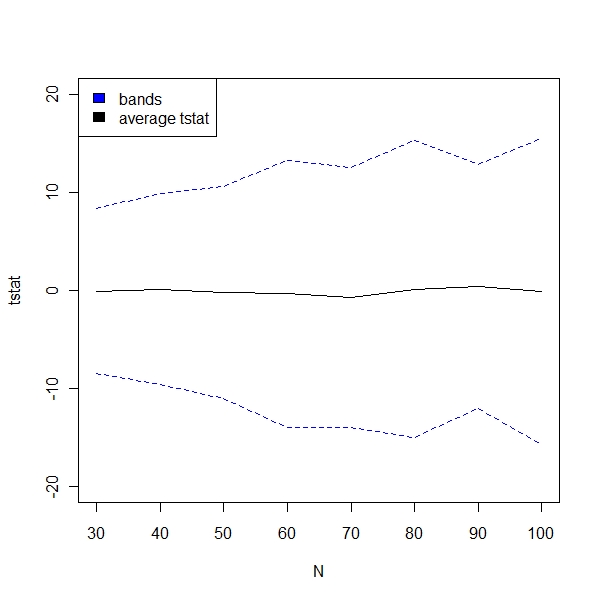

> plot(N, (tstat), type = "l", ylim = c(-20, 20), ylab = "tstat")

> points(N, (tstat) + 2 * (tstat.sd), type = "l", lty = "dashed",

+ col = "blue")

> points(N, (tstat) - 2 * (tstat.sd), type = "l", lty = "dashed",

+ col = "blue")

> legend("topleft", legend = c("bands", "average tstat"), fill = c("blue",

+ "black")) |

t stat shows no sign of converging

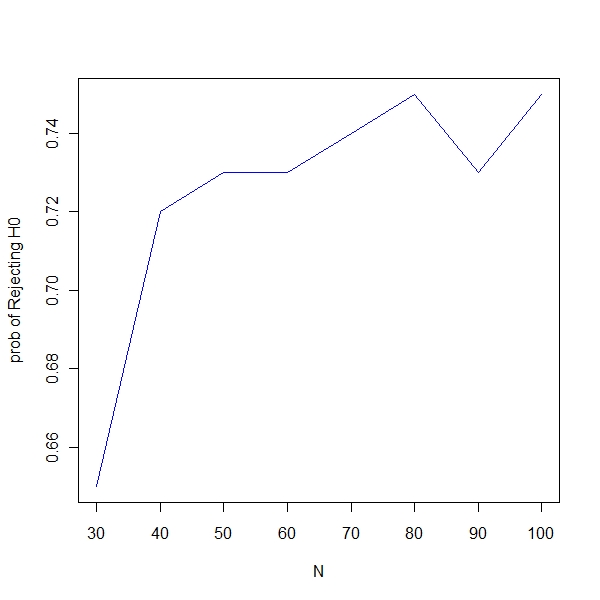

> plot(N, probs, type = "l", , ylab = "prob of Rejecting H0", col = "blue") |

Probability of rejecting null increases even though it is spurious reg